Payment brands are often framed as purely functional, shaped by speed, security, and access rather than identity or emotion. The data, however, suggests that for Gen Z, personal connection matters a lot to the strength of a brand and its contribution to business outcomes.

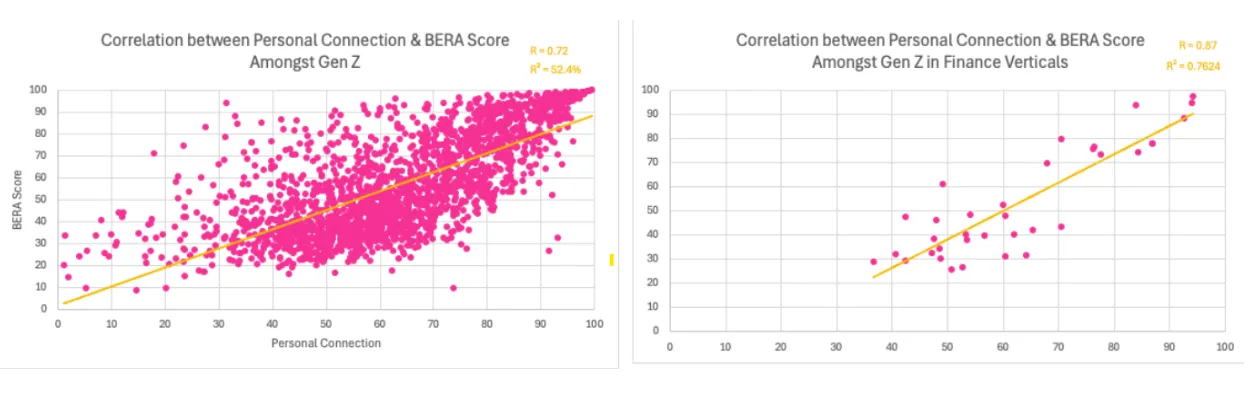

BERA’s analysis across more than 2,000 brands shows that among Gen Z, Personal Connection explains more than half of the variance in overall brand equity. Even more striking, it accounts for more than three-quarters of the variance in equity for finance, banking, and digital wallet brands. For these brands, Personal Connection is one of the strongest measurable signals of brand strength among Gen Z.

To be clear, the data confirms that emotional relevance does not replace functional competitiveness as a driver of brand strength in the financial sector. Instead it highlights that for Gen Z, the functional and emotional reinforce each other, especially in categories like Payments, where the consumer experience is both frequent and high-stakes.

But what is “Personal Connection”?

The data on dozens and dozens of financial brands shows a measurable linkage between the personal connection Gen Z has with such brands and their perceptions of whether the brands feel integrated into their life, aligned with their values, and worthy of ongoing engagement.

Personal Connection is a key driver of brand strength for the major digital wallet brands Zelle, Venmo, PayPal, Amazon Pay, and Apple Pay. Gen Z is not evaluating digital wallets solely as interchangeable utilities; they are assigning meaning to them in the form of a connection that turns a digital wallet from a tool into an everyday essential, which is exactly the type of shift that tends to strengthen loyalty over time.

This behavioral shift is reinforced by broader cultural signals. Research from The Harris Poll finds that more than half of Gen Z consumers now use physical cash only as a last resort, and nearly one in three describe cash users as out of touch. Digital payment methods offer more than convenience for this generation, as they align closely with how young consumers prefer to manage money, monitor spending, and reflect their financial identity in everyday life. In that context, digital payments become part of self-expression and lifestyle alignment rather than just infrastructure.

Equity and Connection: What the Data Reveals

Brand equity among the five digital wallets listed above reinforces the importance of Personal Connection. PayPal enjoys brand equity that is stronger than 95% and 90% of the top 2,000 brands in the U.S. PayPal also performs the strongest on Personal Connection compared to Apple Pay, Venmo, Amazon Pay, and Zelle, whose brand equity are, respectively, in the 90th, 84th, 78th, and 67th percentile. In other words, it’s no coincidence that the brand with equity leadership is winning on personal relevance, meaning, and emotional resonance among Gen Z.

Again, digital wallets still have to meet the basics. They must be user-friendly, intuitive, and capable of meeting consumer needs without friction. These functional expectations are not negotiable. Even the highest Personal Connection score cannot make up for an app that doesn’t work.

However, in a category where the functional baseline has become increasingly commoditized, the source of differentiation is increasingly in the emotional and experiential layer. This is why Personal Connection correlates so strongly with brand equity. When a wallet is both easy to use and feels aligned with the consumer’s daily life, the relationship is stronger.

All this goes to say that, as digital wallets continue to move from occasional tools to routine financial companions, the brands that feel personally connected will be the equity leaders. Relying solely on functional competence is unlikely to build durable loyalty with Gen Z.